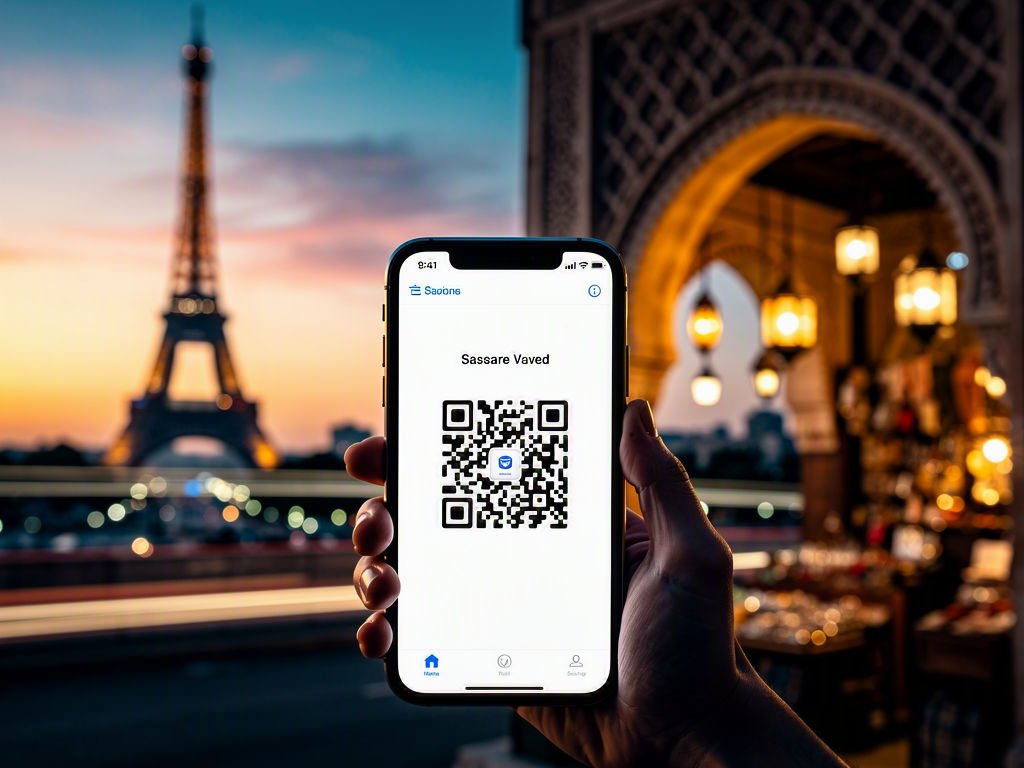

At the base of the Eiffel Tower, a tourist from Bengaluru scans a QR code on the official ticketing site and pays for her entry exactly the way she’d pay for parathas at a roadside dhaba back home: through UPI. No currency-conversion screen, no “insufficient forex balance” alert, no line at a counter that only takes euros. France became the first European stop in UPI’s international expansion in February 2024, when NPCI International tied up with French payments provider Lyra to wire the tower’s ticketing system into India’s rails. As of this month, the same connection runs through Charles de Gaulle airport and several other French locations.

The tower is one data point in a much larger map. UPI now works, in some functional form, in close to a dozen countries beyond India: Bhutan, Nepal, Sri Lanka, Singapore, the UAE, Qatar, Mauritius, Cambodia, and now France. The texture changes country to country. In the UAE, Network International wired UPI into more than 200,000 point-of-sale terminals across 60,000 merchants, from Dubai Mall counters to neighborhood restaurants, on top of Mashreq Bank’s NEOPAY and the local AANI network. Singapore has over 12,000 merchants on board through local payments firm HitPay, up from roughly 9,000 a year ago. Nepal was the first country to run UPI as core payment infrastructure rather than a tourist add-on.

For the diaspora, the more consequential change happened quietly in January 2023, when NPCI let banks onboard NRE and NRO accounts onto UPI using international mobile numbers, no Indian SIM required. An NRI in Toronto or Melbourne can now link an Indian bank account directly to a UPI app on a Canadian or Australian number, and pay a landlord in Kochi or settle a wedding vendor’s bill in real time, the way anyone standing in India does. It closes a gap that had quietly persisted for years: a system built to erase friction inside India had, for a long stretch, simply locked out anyone who’d left.

The traffic runs the other direction too. Under a program called UPI One World, travelers from G20 countries can get a prepaid wallet activated on UPI after a passport-and-visa KYC check at the airport, loaded with rupees off a foreign card, without ever opening an Indian bank account. It’s a quiet reversal: for over a decade, visitors to India dealt in cash or card surcharges at every counter. Now someone landing from Tokyo or Toronto can be tapping into the same rail as the chaiwala outside their hotel within fifteen minutes of clearing immigration.

The volumes underneath all this are hard to hold in your head. NPCI puts UPI at more than 23 billion transactions a month domestically as of May 2026, worth close to $312 billion, a figure industry trackers place at close to half the world’s real-time payment volume. Transaction counts have compounded at roughly 46% a year since 2017-18, when the entire system cleared under a billion transactions annually. It clears that most weeks now.

That scale is exactly why other governments keep signing on. Writing in Diplomatist, analyst Pitamber Kaushik frames UPI’s real export value as “credibility, the currency of influence.” His argument: India isn’t selling a finished product so much as a working blueprint, interoperable rails and low friction that let competing private apps sit on shared public infrastructure instead of one company owning the plumbing. As UPI’s international expansion continues, NPCI is reportedly in talks with more than 30 countries and has floated a target of 20 nations running UPI-linked rails by 2028-29. Malaysia’s DuitNow system was the latest name added to that pipeline, with integration reported this past February.

It’s worth being precise about what’s actually crossed the border, though. UPI abroad still settles in rupees; it isn’t a foreign-exchange platform, and an NRI’s linked account still has to be funded in INR. A resident paying at a Dubai Mall counter is really extending an Indian bank balance across a border, not creating a new currency corridor. The feeling of “the same app, everywhere” undersells the plumbing behind it: separate bilateral deals, separate KYC regimes, separate limits, city by city.

What doesn’t need translating is the smaller, almost boring feeling it produces. Ask an NRI who’s paid a Kochi landlord from a Toronto number, or a tourist who bought an Eiffel Tower ticket without hunting for a currency counter, and neither describes it as diplomacy. They describe it as not having to think about money for one extra second, which, for a generation that grew up watching parents wire funds home through agents and paperwork, might be the quieter revolution.

Sources

- Republic World — Digital India Goes Global: Bharat’s UPI Now Fully Operational at France’s Iconic Eiffel Tower, July 8, 2026

- Business Standard — Now, pay for Paris’ Eiffel Tower visit through India’s UPI, says NPCI, February 2, 2024

- Gulf News — UPI payment system now accessible to Indian tourists in over 60,000 outlets across UAE

- Business Standard — NPCI’s international arm partners with Singapore firm to expand UPI, March 2025

- SBNRI — UPI for NRIs: How to Use UPI Abroad with an International Number

- Zeebiz — UPI: How foreign nationals and NRIs visiting India can make payments using UPI

- Diplomatist — How UPI Can Become India’s Next Soft-Power Export

- IBEF — UPI Transactions Soar to Record US$312.21 billion in May 2026

- Coinlaw — UPI Statistics 2026: 23.2 Billion Monthly Transactions and 49% of Global Real-Time Volume

SEO

- SEO title: UPI International Expansion: From India to Nine Countries

- Meta description: UPI’s international expansion now spans the Eiffel Tower, Dubai malls, and NRI bank accounts abroad. Here’s what’s actually changed for the diaspora.

- Focus keyword: UPI international expansion

- Secondary keywords: UPI for NRIs abroad, UPI countries list 2026

- Slug: upi-international-expansion-diaspora

- Category: Culture & Diaspora

- Tags: UPI, NRI, South Asian diaspora, digital payments, India fintech, remittances